Households Are Extremely Illiquid

Understanding That Americans Have Little Savings is Critical to Understanding the American Economy

The views expressed in this blog are entirely my own and do not necessarily represent the views of the Bureau of Labor Statistics or the United States Government.

“Illiquidity”, meaning an inability to quickly obtain sufficient cash or cash equivalents, is usually a term reserved for businesses and financial markets. During the financial crisis of 2008, the repo crisis of 2019, and the recession of 2020, policymakers desperately worried that big banks and businesses would suffer from harsh illiquidity and would be unable to meet their short-term obligations. Insolvency can come immediately after illiquidity as companies who cannot meet short-term obligations become bankrupt even if their long-term prospects were sound. While American companies can suffer from illiquidity crises during times of economic and financial strain, American households virtually always stare down the threat of a thousand small liquidity crises. They have little savings, few debt financing options, and the options they do have come with punishing interest rates or personal costs. Understanding how Americans would react to an emergency that would cut off their income is critical to understanding the American economy.

Household Illiquidity

The Federal Reserve publishes the Survey of Household Economics and Decisionmaking, a wide-ranging survey on consumer finances and behaviors, every year. It is one of the most comprehensive and detailed publicly-available household surveys, making it an important tool to analyze household finances.

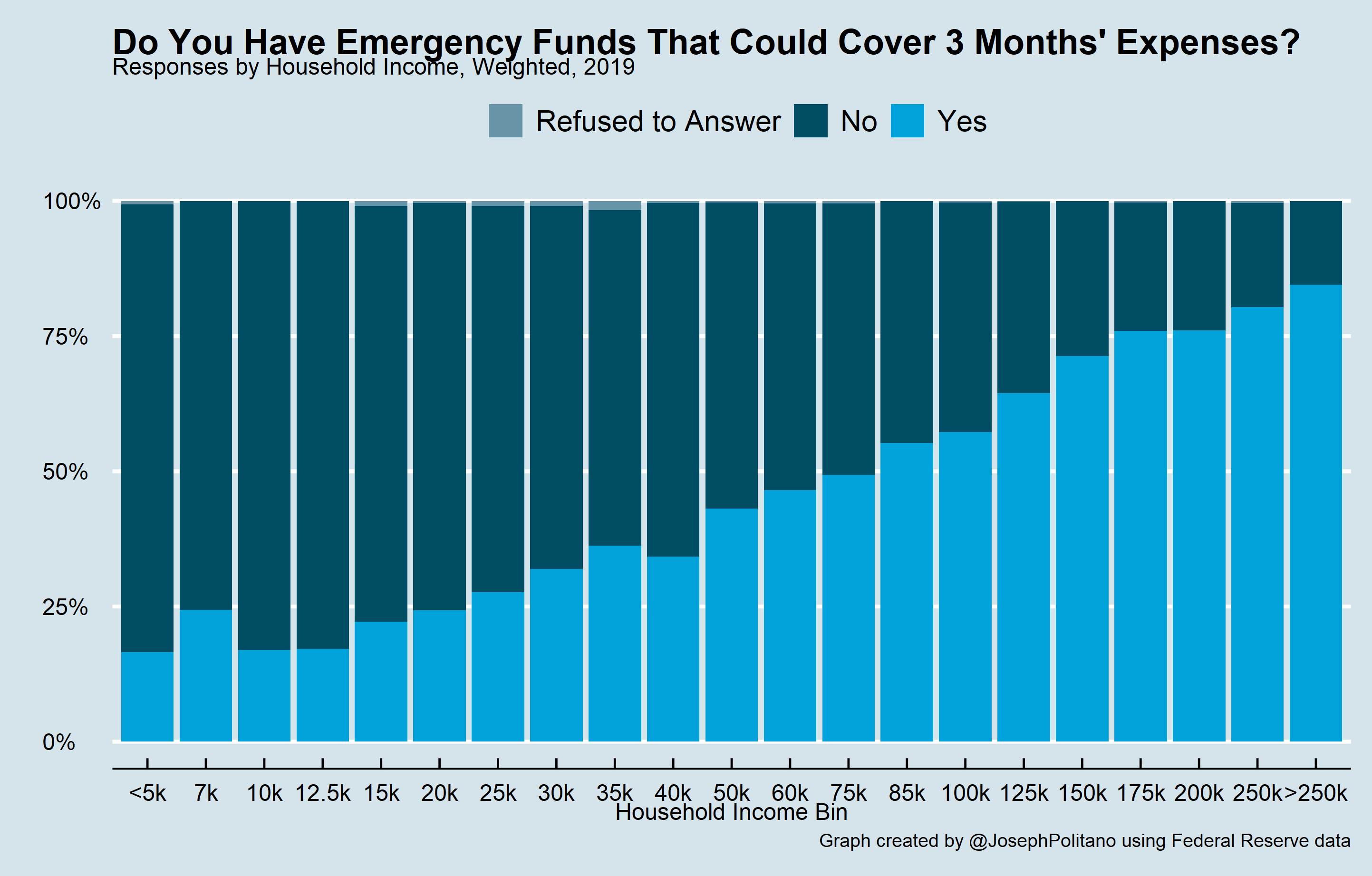

Personal finance experts usually recommend to keep an emergency fund worth 3-6 months worth of expenses in case you lose your job or run into a large unplanned expense. However, as shown in the chart above, the majority of Americans do not even have the basic 3 months’ worth of emergency expenses saved up. This is even more pronounced among low-income households, where extremely few people report having sufficient emergency funds. While there is an extremely clear positive correlation between household income and having a 3 month emergency fund, it is also remarkable the degree to which many high-income households do not have emergency funds. Approximately 1/4 of households making between $175,000 and $200,000, almost three times the median household income, do not have sufficient emergency funds.

In a follow up question, the Federal Reserve asks respondents who did not have a 3 month emergency fund if they could cover those emergency expenses with a combination of savings, borrowing, and selling assets. The graph above shows the share of total respondents who answered “no” to that question, meaning they believe they have no way of covering three months of expenses. At the median household income, more than a quarter of households fit this description, and the proportion only gets higher as household income decreases. The graph above also demonstrates that, while many high-income households do not have an emergency fund, few believe that they would be unable to come up with 3 months’ expenses at all.

When excluding retirees, the situation looks marginally worse. The graph above is the same as the prior graph but only including people who did not self-identify as retired. At almost every household income lower than $100,000-$125,000, non-retirees are slightly more likely to be unable to cover 3 months’ expenses than people on the whole, although the difference is likely insignificant.

If you have ever encountered headlines saying that a large percent of Americans could not pay a $400 emergency expense, that data also comes from the Survey of Household Economics and Decisionmaking. The graph above plots how households would pay for that hypothetical $400 emergency against their household incomes. Respondents are able to select multiple answers, so it is worth noting that the percentages in the graph above are a percent of all answers, not a percent of households.

The results here point to several important conclusions. First, low income households rely disproportionately on borrowing from friends/family and selling their belongings. Second, as their incomes increase households are less likely to be completely unable to pay for $400 emergency expenses and are also less likely to rely on borrowing. Finally, households in general have little savings and are likely to go into debt or otherwise struggle in the face of an emergency. Among households making $35,000-$40,000, for whom a $400 expense is only 1% of their annual income, less than 50% of responses indicated they would pay with cash or with a credit card paid off next statement cycle. This is especially important because of the punishing interest costs Americans can incur when borrowing on a credit card or through payday loans. While few Americans report that they would go into debt with a private lender, when push comes to shove many of the households who cannot pay a $400 expense will end up stuck in debt.

While it might feel natural to moralize about Americans’ lack of savings, the reality is that these are behavioral and structural phenomena just as much as individual phenomena. When nearly one quarter of households making $175,000-$200,000 a year, almost the top 10% of household incomes in one of the richest countries in the world, do not have a three month emergency fund the issue must go beyond personal failing. For one, most households have the bulk of their wealth tied up in houses and retirement accounts, which are illiquid capital goods that policymakers give favorable treatment to. Secondly, human beings are also not behaviorally hard-wired to make complex forward-looking financial decisions, especially in a system where corporations are deliberately appealing to the processes that are behaviorally hard-wired in order to increase sales. Finally, when households increase their incomes they tend to increase their recurring expenses: buying a bigger house, adding another car, shopping at pricier restaurants, etc, leaving them almost as illiquid even as before their incomes increased.

While we should work to lower household illiquidity as much as we can (if you have not already, there is nothing I can recommend more than starting a 3 month emergency fund), it is not likely that we could solve the household illiquidity problem in aggregate. Understanding the implications of this illiquidity on macroeconomics is therefore critical in making informed predictions about economic trends and the impacts of public policy.

Macro Implications

What does it mean for the American economy that most American households have little liquid savings? For one, it means that even short interruptions in regular income can result in catastrophic collapse for many families. If households lose their primary sources of income they will rapidly be unable to meet their current obligations and will become delinquent on important bills, with large effects in the broader macroeconomy. During recessions households where members lose their jobs rapidly risk of running out of savings and becoming insolvent, even if their long term finances are still secure. The knock on effect of this is lower spending, more delinquent loans, lower business/corporate income, and additional unemployment. This self-reinforcing cycle of increased unemployment mixing with illiquidity to cut aggregate demand and increase unemployment results in an accelerating recession that can wreck the economy if left unchecked.

Indeed, that is the principal mechanism by which the 2008 recession accelerated. After tight monetary policy and coupled with systemic financial risk kicked off the crisis, a cycle of unemployment accelerated it dramatically. Unemployed workers could not pay their bills, leading them to become delinquent on debt and, in many cases, go bankrupt entirely. As households stopped paying their bills, consuming, and investing businesses lost large chunks of their income. This slowed money supply growth, decreased aggregate demand, and further amplified the crisis.

The chart above compares the delinquency rates for single family residential mortgages and credit card debt during the 2008 and 2020 recessions, indexed to 1 quarter before the recession. In the 2008 recession, the percent of single family mortgages in delinquency tripled in the two years after the recession and credit card delinquencies remained elevated. In 2020, however, mortgage delinquencies increased only slightly and credit card delinquencies decreased. Why is that?

In the wake of the 2020 recession, the federal government undertook significant efforts to protect household incomes and prevent the kind of “household liquidity crisis” that took over in 2008. As the chart above shows, the majority of Americans quickly spent their stimulus checks or used them to pay down prior debt, exactly in line with the expected behavior of illiquid households. The enhanced unemployment insurance, as I wrote about last week, was also critical in preventing short-term income gaps from being catastrophic for households and the economy in general. In addition, the federal government took deliberate steps to institute rent relief, mortgage forbearance, and student loan forbearance programs designed to ensure that people could wait until their financial situations were secure before having to worry about their bills.

Conclusions

Analyzing and modeling economic flows is essential for understanding the behavior of economic participants and the economy in general. Whenever you’re evaluating economic data and policy changes, keep in mind that the majority of households have little in the way of liquid savings and are likely to spend most of their income.

With this in mind, public policy must be structured to preserve income in the event of crisis. This means strong automatic stabilizers, countercyclical fiscal policy, and fast-moving federal departments. Policy should also ensure that people are provided for during their non-working years. After all, if people generally struggle to save 3 months’ emergency funds then they will struggle even more to save for retirement or for their children. Finally, economists and economic analysts should ensure that their models, when appropriate, account for the irrational illiquidity that occurs in real life households.