America's Electricity Gap

US Power Investment is at Record Highs, Driven by a Solar & Battery Boom. It's Still Not Enough to Meet Demand Growth.

Thanks for reading! If you haven’t subscribed, please click the button below:

By subscribing, you’ll join over 80,000 people who read Apricitas!

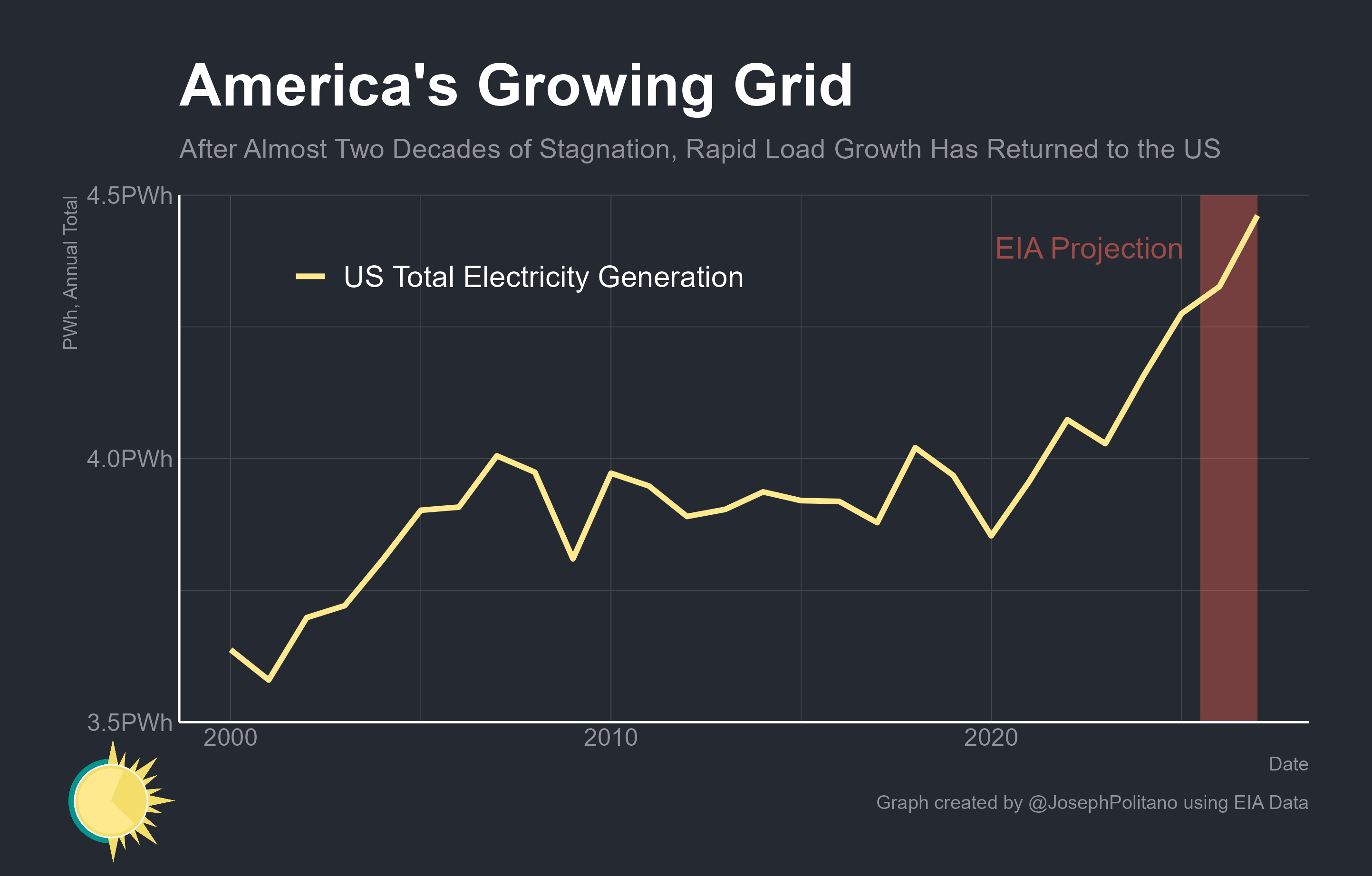

America has entered another era of electrification—US power consumption has risen more in the last two years than over the previous 15 combined. Yet this hasn’t been nearly enough to meet demand, with electricity prices also rising more over the last 4 years than the prior 14. Demand from AI, heavy industry, heating, and transport is driving load growth but also outstripping growth in power infrastructure—leaving America with an increasingly large electricity gap that’s driving up prices. Projections from the US Energy Information Administration (EIA) expect generation to accelerate slightly over the next two years, growing another 4.6% in total, but that’s still not quick enough to close the gap or prevent further price appreciation.

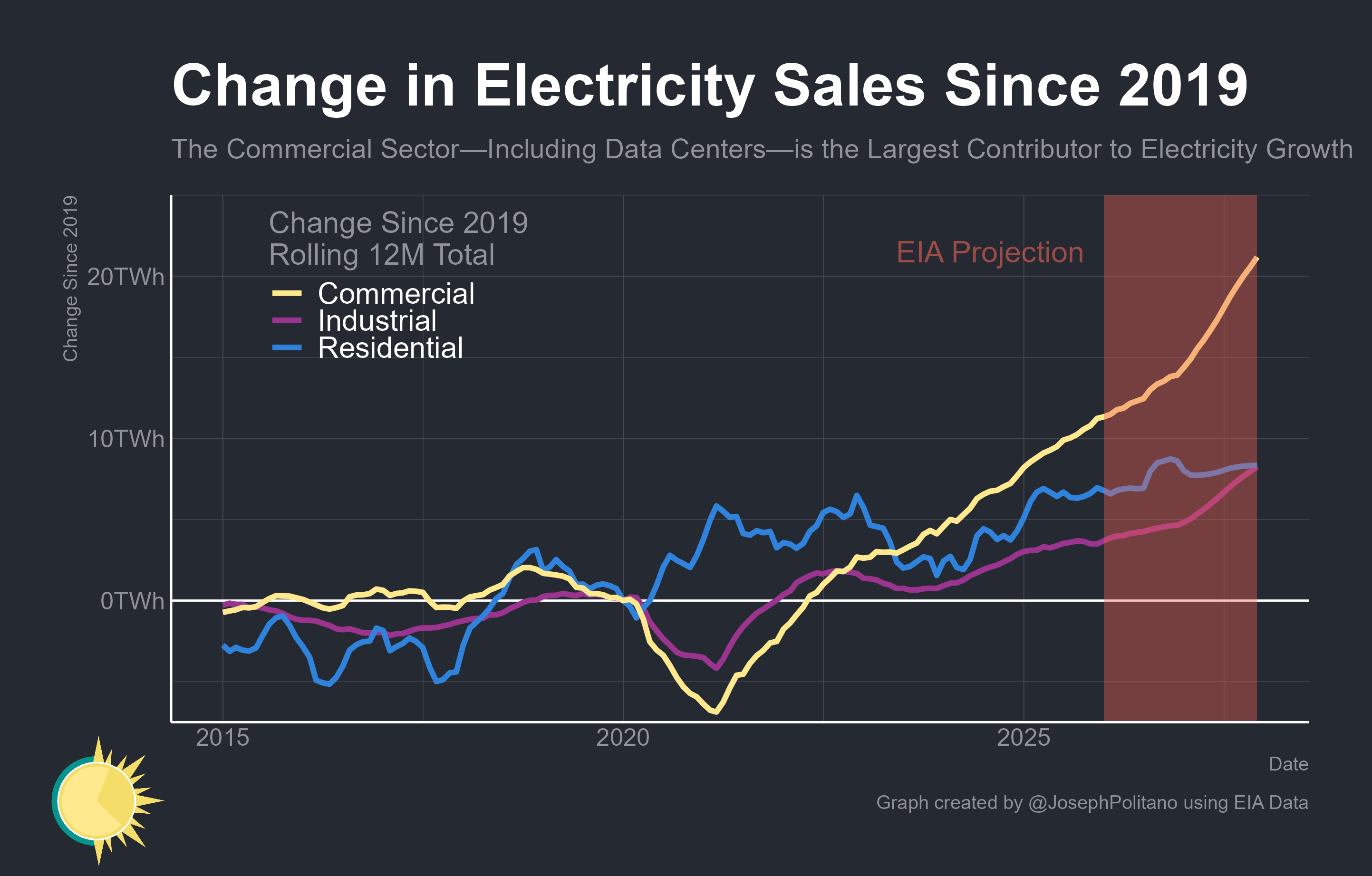

The return of sustained load growth after more than a decade and a half of stagnation represents a fundamental change in America’s energy markets, with the source of rising demand shifting alongside its scale. Indeed, the EIA expects more upcoming load growth to come from commercial entities—a category that includes data centers—than from industrial and residential uses combined. If those projections hold true, commercial power consumption will have grown more in the 4 years since ChatGPT’s launch than in the two decades prior.

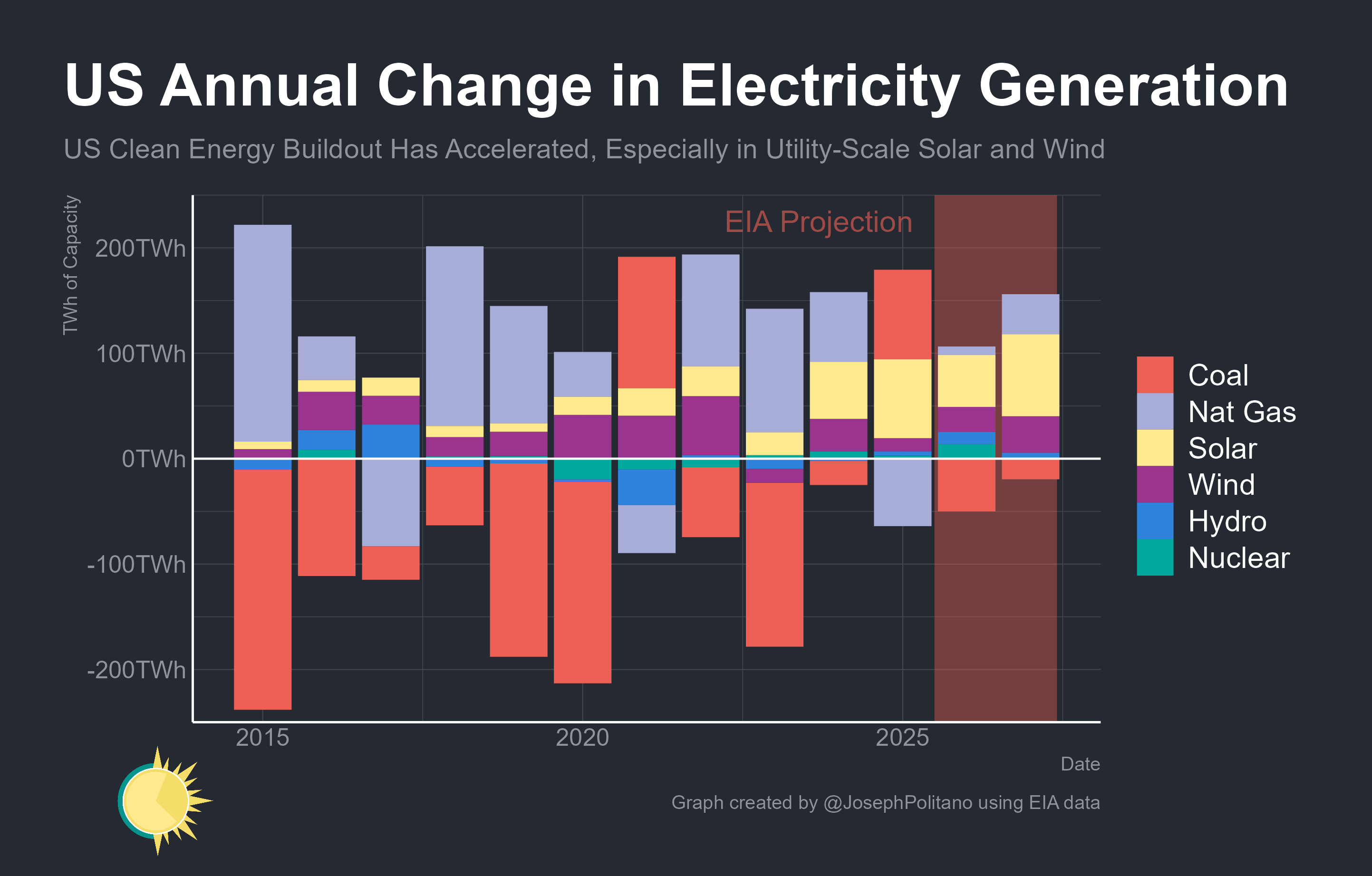

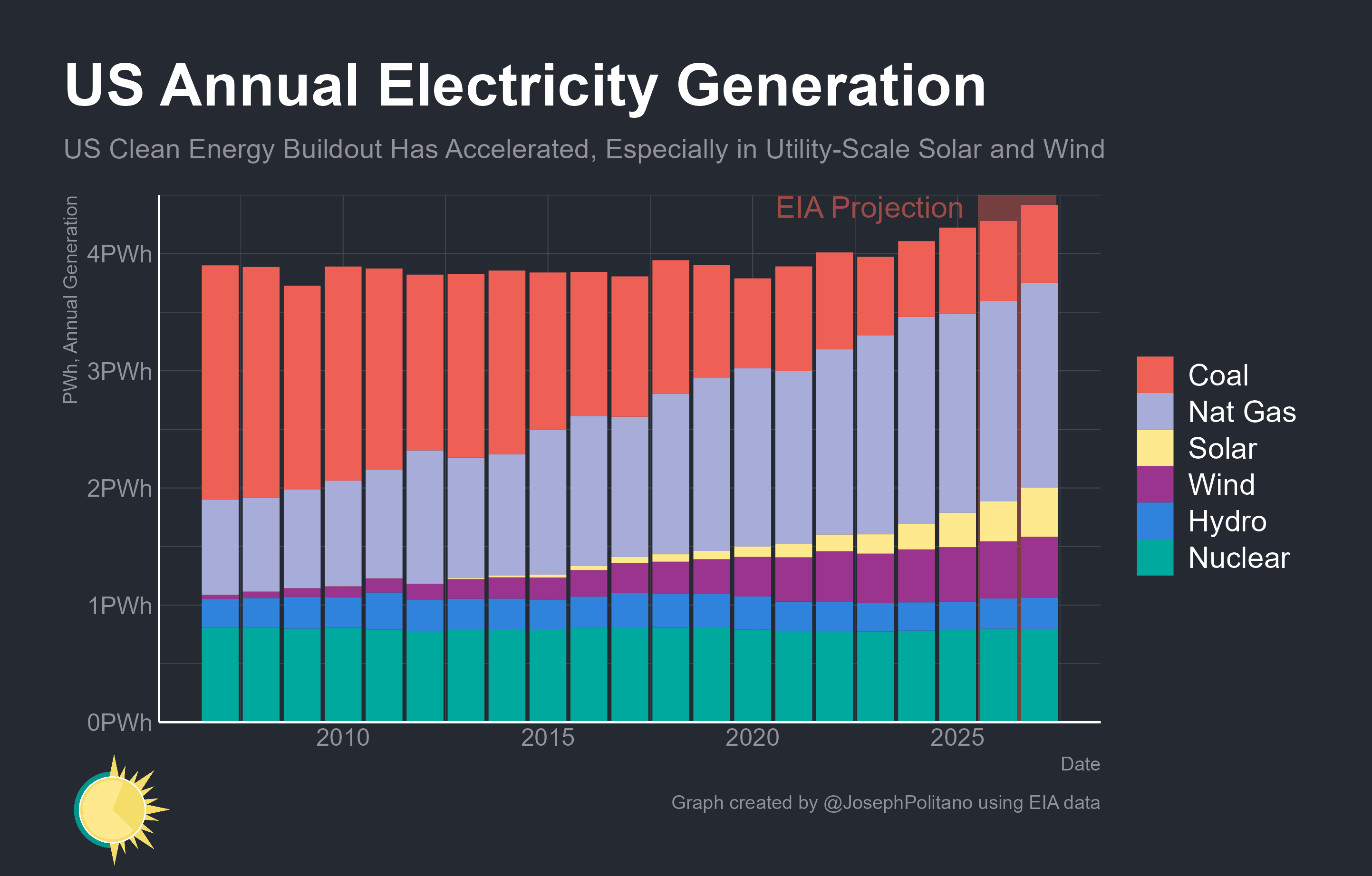

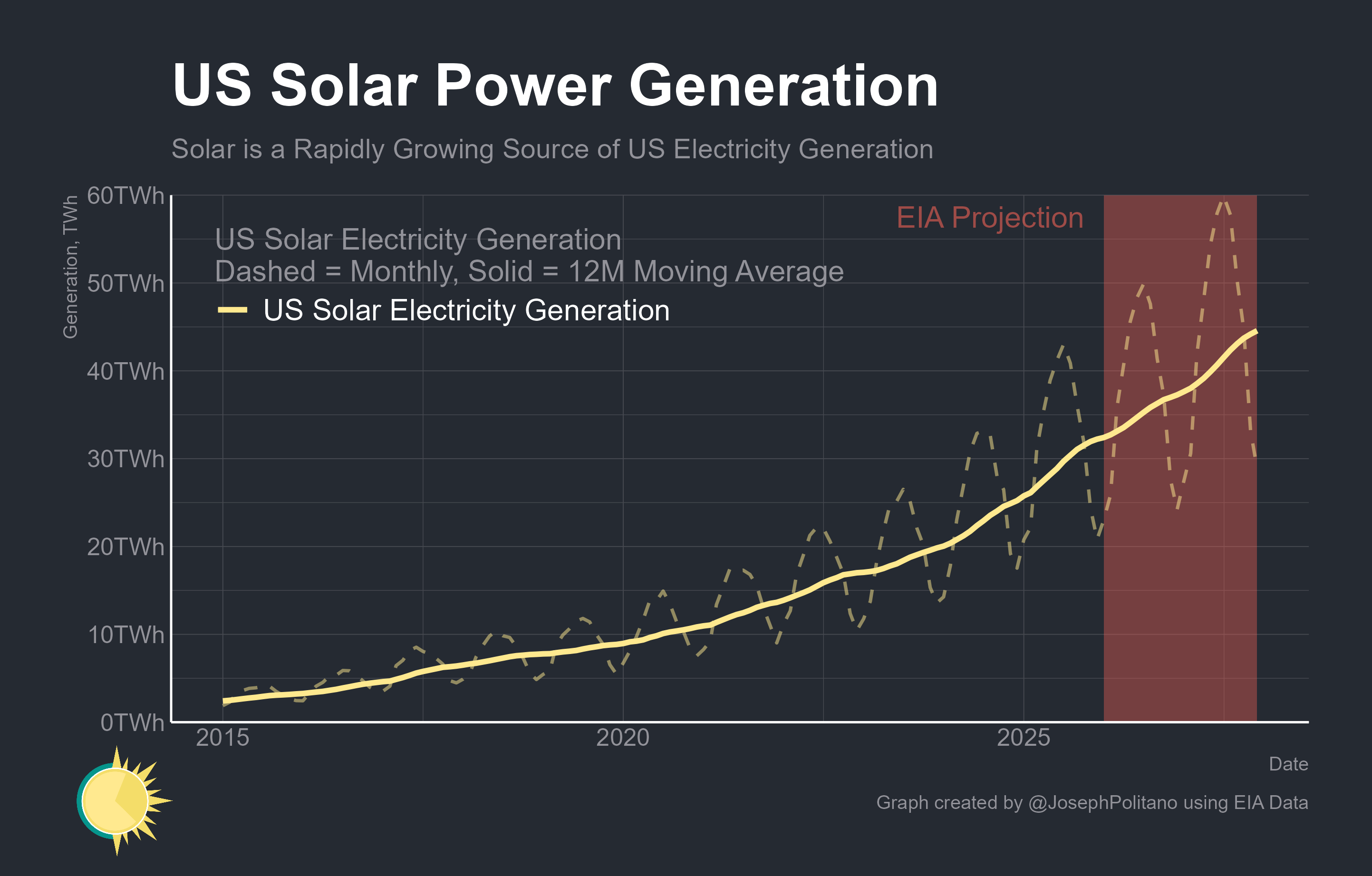

The second fundamental change in electricity markets is how the US is meeting the new rise in power demand—by deploying record amounts of renewable energy, primarily solar and batteries. 2025 saw the largest year-on-year increase in US solar generation on record, with total solar power rising 28% to 389TWh. That’s despite the Trump administration cutting subsidies to wind and solar production, cancelling permitting approvals for major projects, and imposing tariffs on many of the sector’s key inputs. Solar power growth is projected to slow slightly this year, though remaining near its 2024 pace, before breaking the growth record again in 2027.

In other words, solar power will be meeting the majority of US load growth for the first time in history. Yet America has fallen significantly behind both China and the European Union in terms of solar energy deployment, even on a per-capita basis. Legacy US coal plants, which have been closing for decades as they’ve been outcompeted by natural gas and solar, are now being retired at the slowest pace since 2010 as grids are forced to keep them online to meet growing demand. America was one of only a few major countries that increased coal power production in 2025, a year when even coal powerhouses China and India reduced their use.

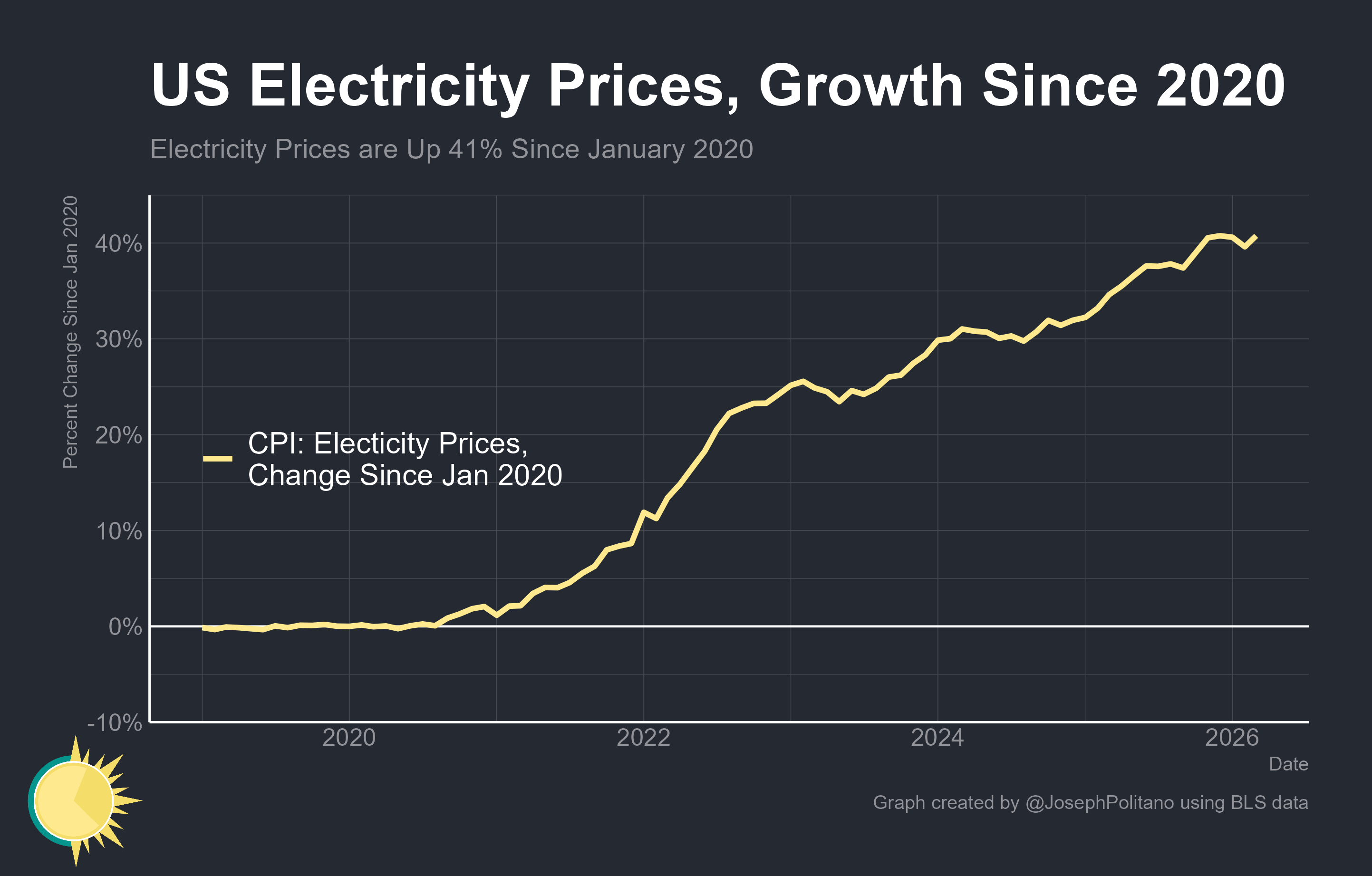

Meanwhile, US residential electricity prices are up more than 40% since 2020 and continue rising. Given the rise in energy demand over the last year and the fossil-fuel price shock caused by the US attack on Iran, prices are likely to increase even further in the near future. That also means the Trump administration’s decision to block major solar, wind, and battery projects now has much higher economic costs. Their decision to exempt computers and other data center inputs from tariffs while hitting key electrical infrastructure like wires, transformers, and batteries further exacerbates the energy crunch.

Yet the fact that renewable energy is still growing rapidly, even in such an unfavorable policy environment, speaks to the scale of the technological acceleration currently underway. Solar and batteries are growing at a record pace throughout nearly the entire globe, increasingly winning on cost and accessibility in the US and in places as politically and economically disparate as Pakistan or Germany. Deploying them faster will be key to closing America’s electricity gap.

America’s Energy Investment Boom

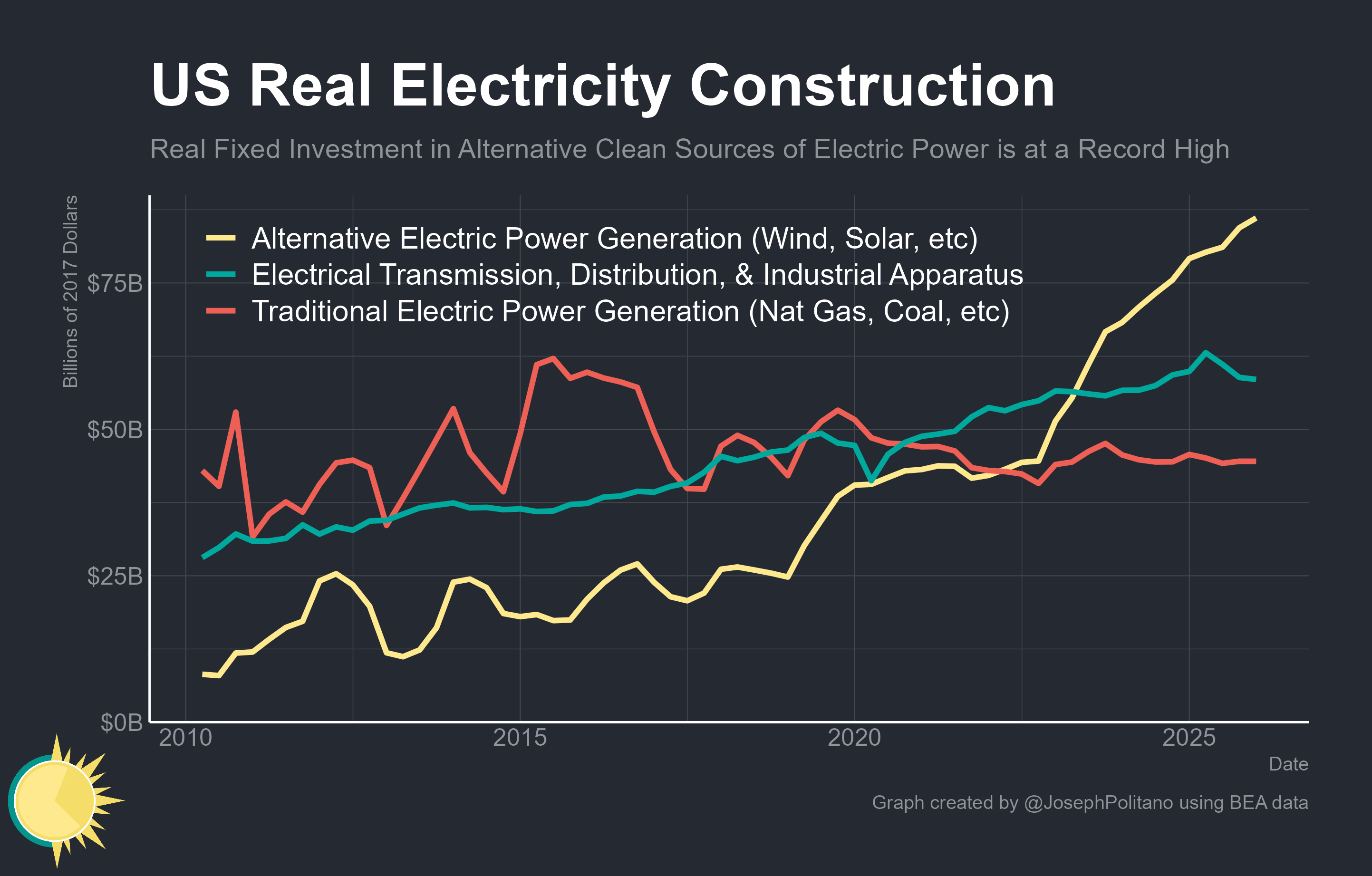

The US is currently investing record amounts into power generation, driven entirely by the rapid growth in “alternative” energy sources like wind and solar. In real terms, the scale of that investment has more than doubled since 2020 and is up more than 10x since 2010. Likewise, investment in electrical transmission and distribution equipment also hit a record high at the start of this year, though it has since fallen back to 2023 levels. Meanwhile, investment in “traditional” electricity generators like natural gas, coal, and nuclear has been essentially flat over the last four years and remains well below its record highs.

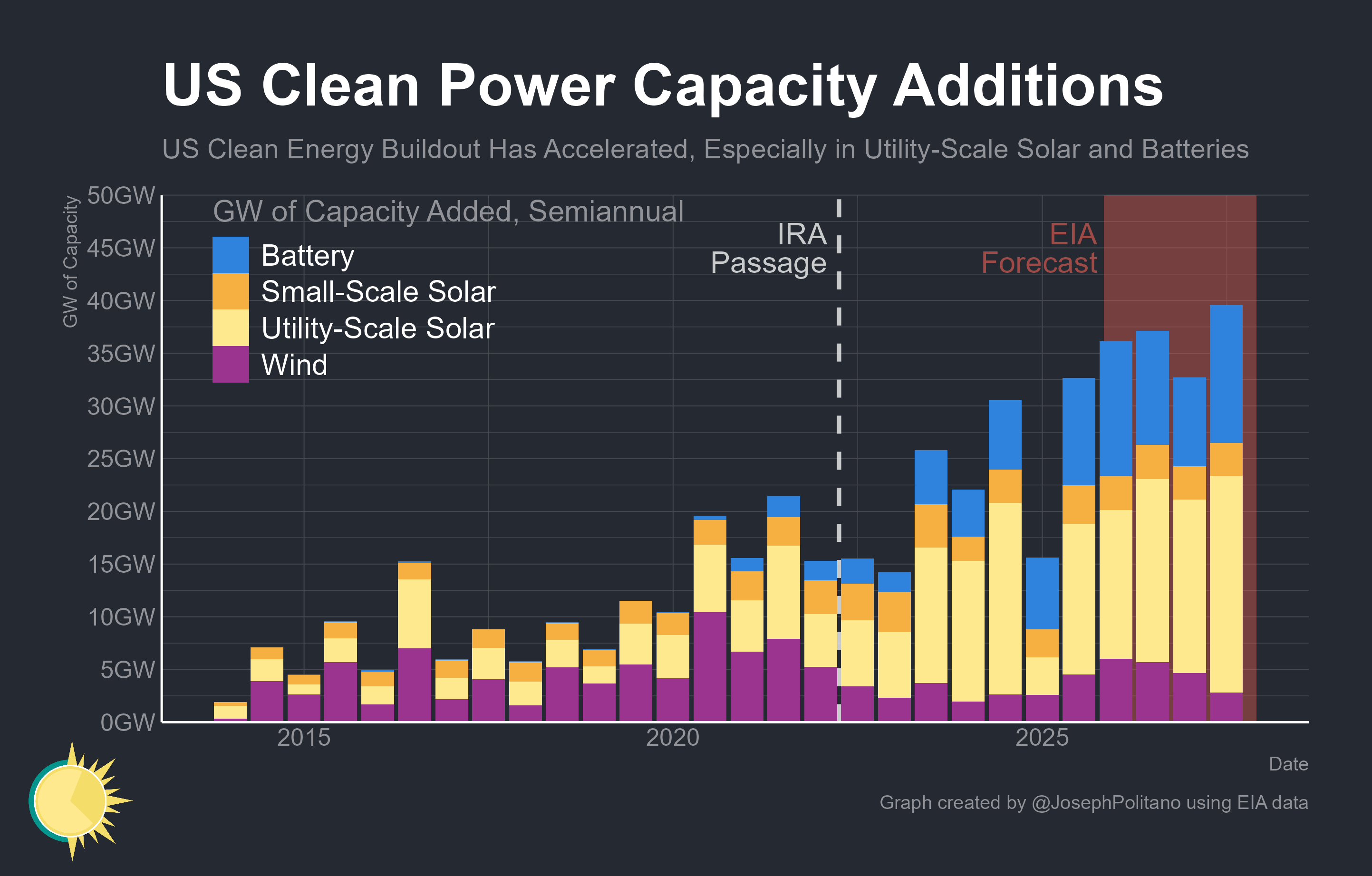

Total US renewable capacity additions took a major hit at the start of 2025 when the Trump administration first returned to office, but rebounded to new record highs in the second half of last year. The EIA projects the US will break that record again over the next two years, primarily thanks to growth in utility-scale solar deployments. Battery additions will also hit record highs to supplement those new solar panels, while wind power additions will rise slightly this year before sinking near post-COVID lows next year.

Of course, power capacity is not power generation, and renewable power sources have lower capacity factors than their fossil-fuel counterparts because they generate less electricity at night, during cloudy days, or when the wind is weak. Yet renewable generation is also at record highs and expected to rise further, due almost entirely to solar. US solar output rose 28% in 2025 and is projected to rise another 16% this year and 20% in 2027. By then, it’ll make up 11.3% of total electricity.

The greatest problem with solar is its temporal inconsistency, with the sun’s output varying by the hour, day, and month. This problem becomes even more acute when solar makes up a larger share of the grid, as electricity becomes overabundant during the daytime and summer but remains scarce at night or during winter. This variability makes short and long-duration batteries an obvious and necessary complement to solar panels.

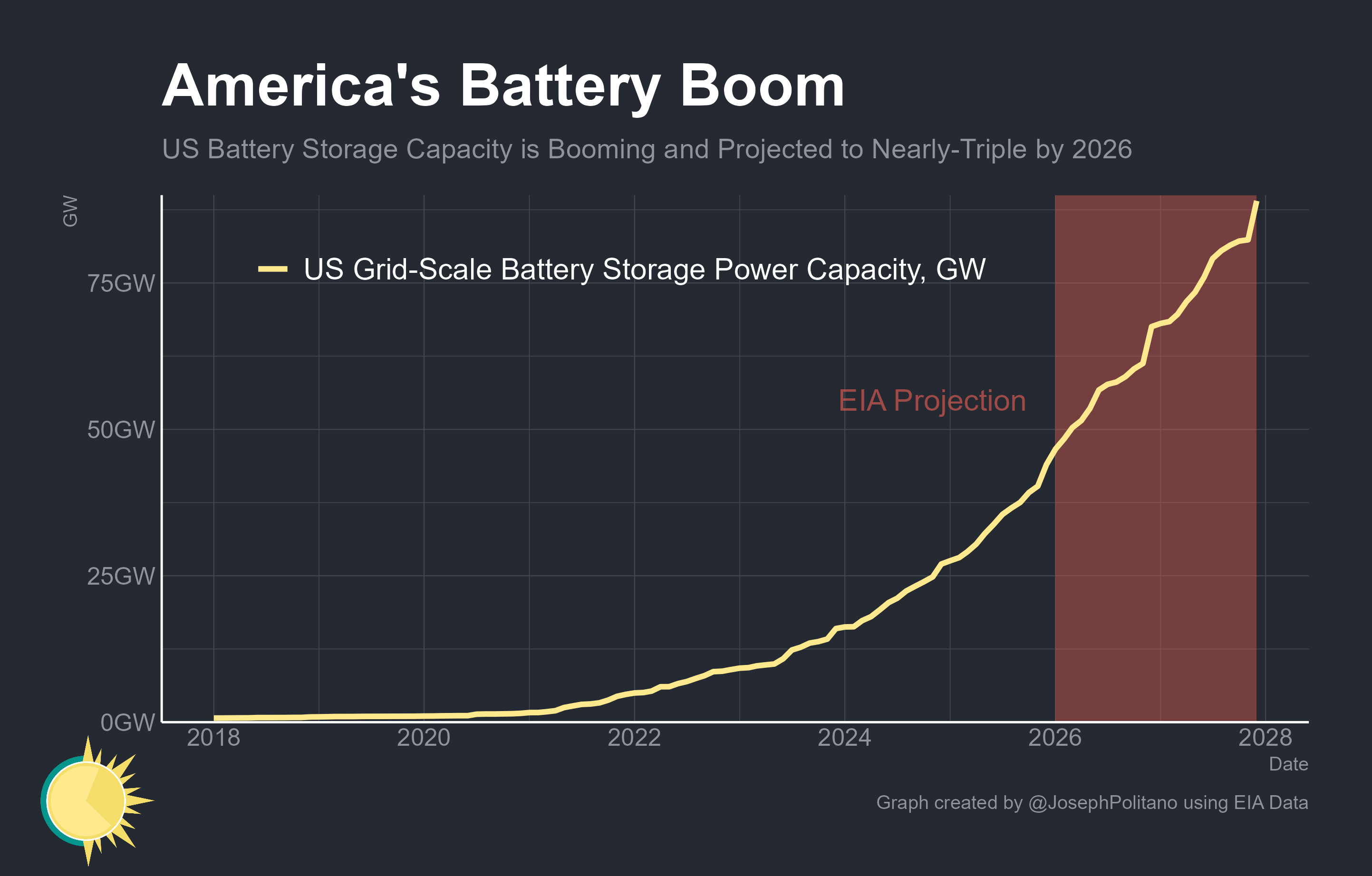

That’s why the US is also building record amounts of utility-scale battery storage, with the pace of additions hitting an all-time high in late 2025 and expected to grow further over the next two years. Total US battery power capacity, which measures the peak amount of electricity deployable at a given moment, is projected to double over the next two years to almost 90GW. Official data don’t provide timely measures of energy capacity (the total amount batteries could supply to the grid through a full discharge), but industry sources also show it rising even faster than power capacity, up more than 55% in 2025.

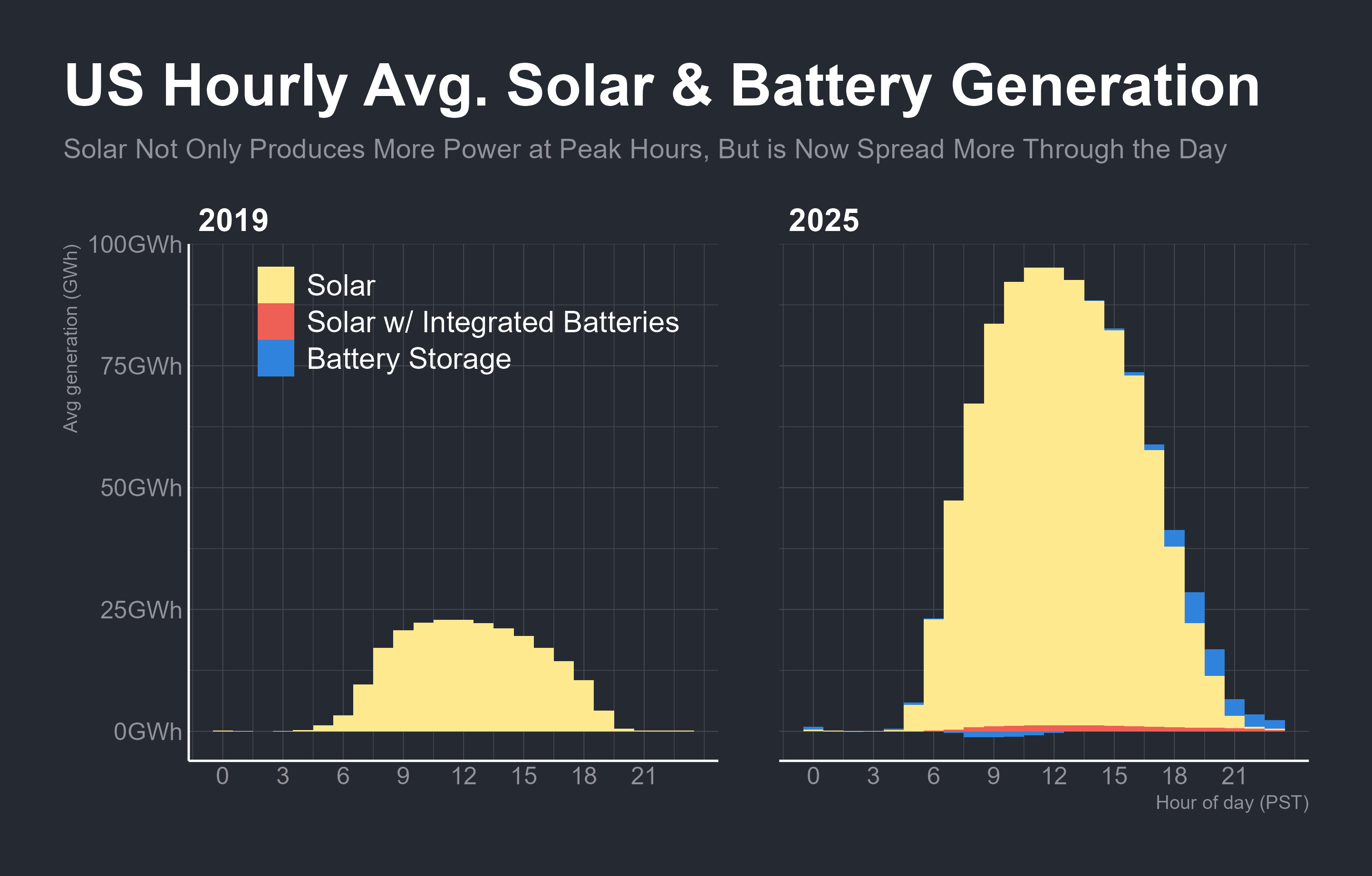

In 2019, there was virtually no utility-scale battery capacity in the United States, and solar only made up about 2.5% of American electricity. Now solar not only provides vastly more electricity during the peak daytime hours but also charges batteries, which then provide additional power near dawn and dusk. Averaging hourly power generation across the entire year, batteries now provide roughly 26.7 GWh throughout the day, with 6.3 GWh delivered in the peak hour alone.

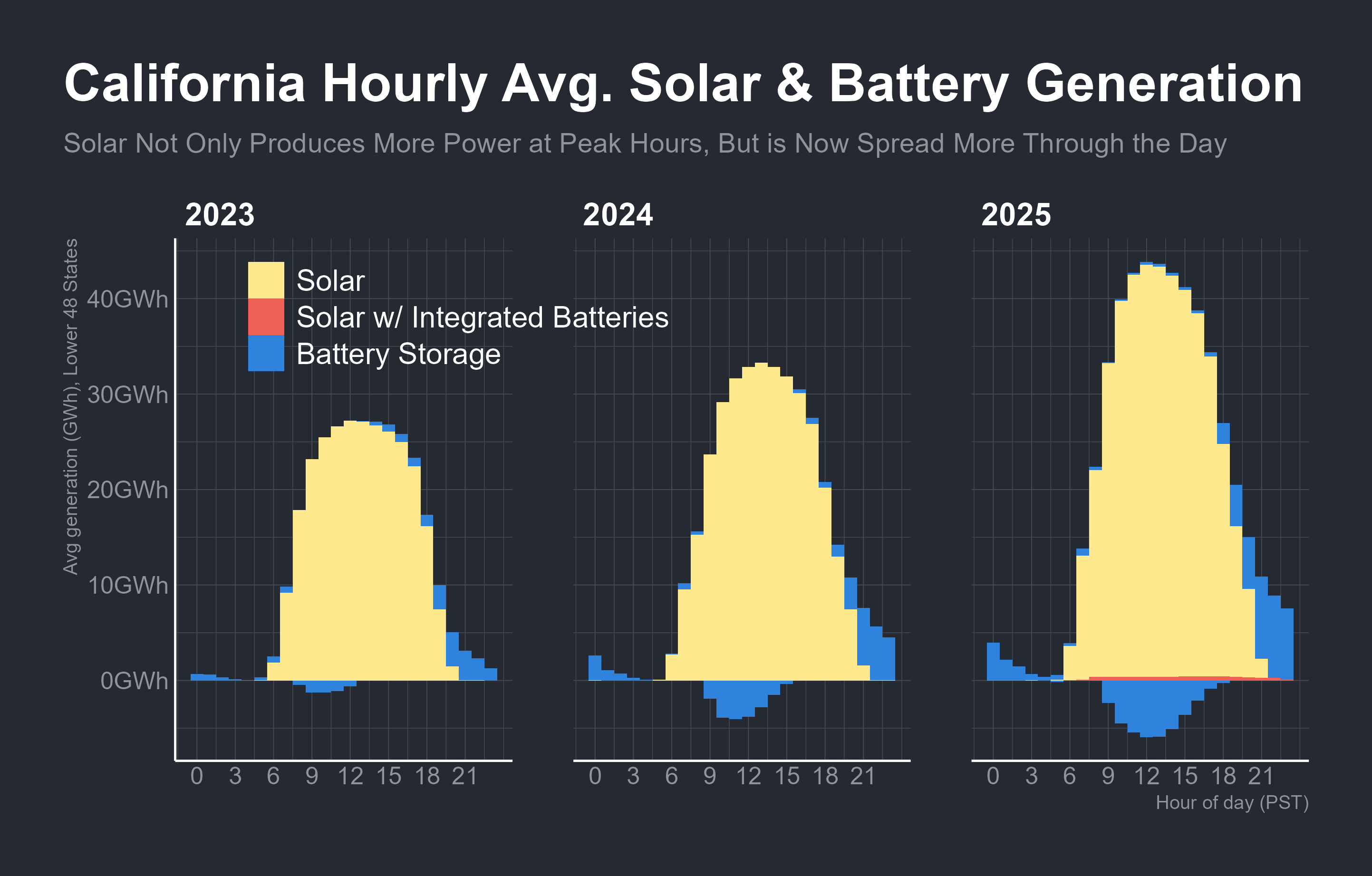

At the scale of the entire country, this is still only a tiny portion of overall electricity, with gross discharges equaling about 0.2% of total electricity consumption. Yet during bright summer days in California, Texas, and some other parts of the US, solar already frequently generates more power than needed to meet all grid demand during midday, charging batteries that meet a significant portion of demand after sunset. That generation pattern will only become more common as solar and batteries both become more widespread throughout the United States in the near future.

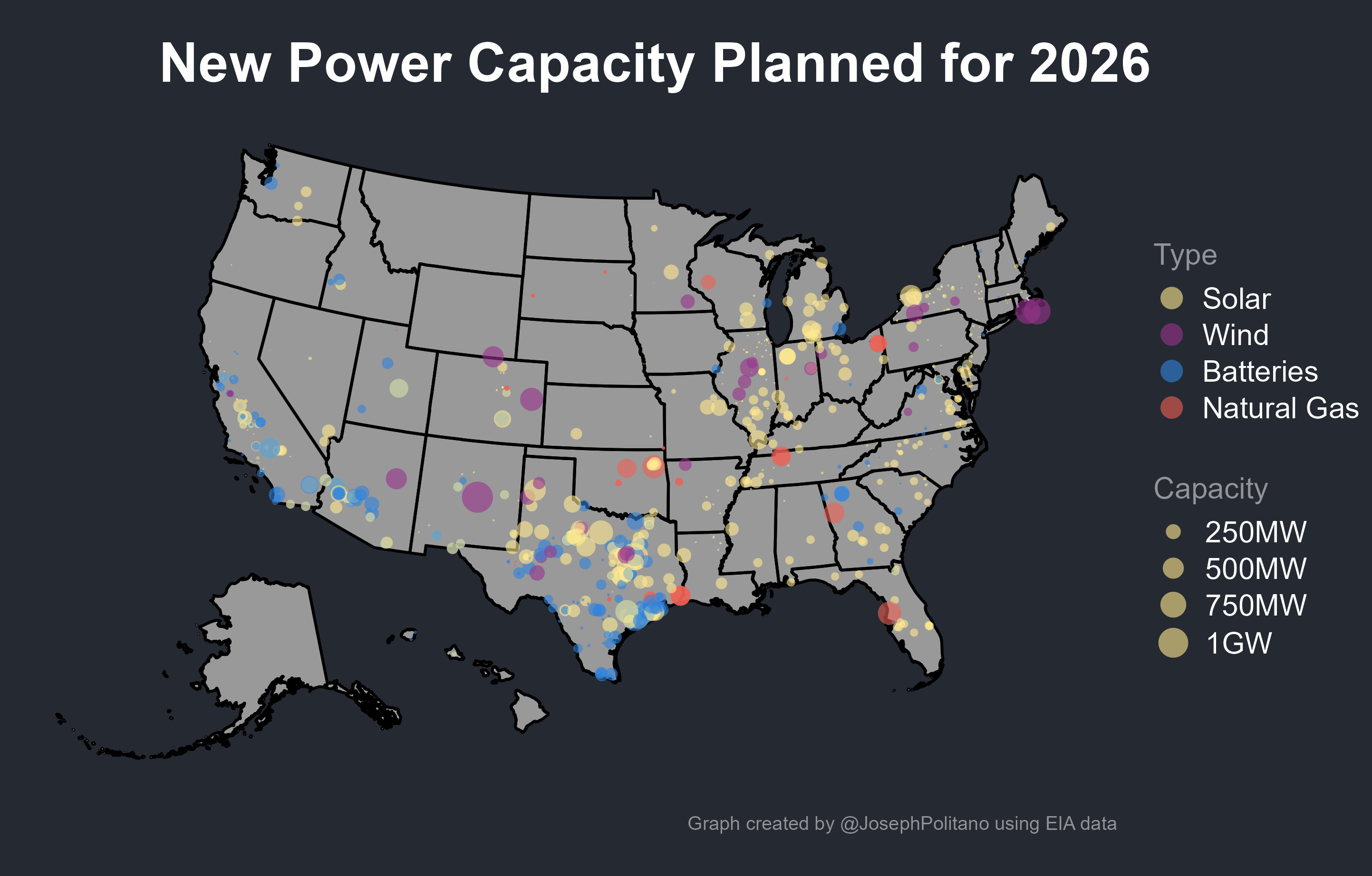

Even more solar and batteries will be built throughout the United States in the near future, with over 40GW of solar and 22GW of battery capacity slated to come online in the next year. Those solar and battery plants are especially concentrated in the sunbelt—with Texas (16GW of solar, 12GW of batteries), California (2.7 GW of solar, 3.2GW of batteries), and Arizona (2.6GW of solar and 3GW of batteries) leading the pack. Texas alone is set to make up 55% of new US battery capacity and 41% of new solar capacity over the next year.

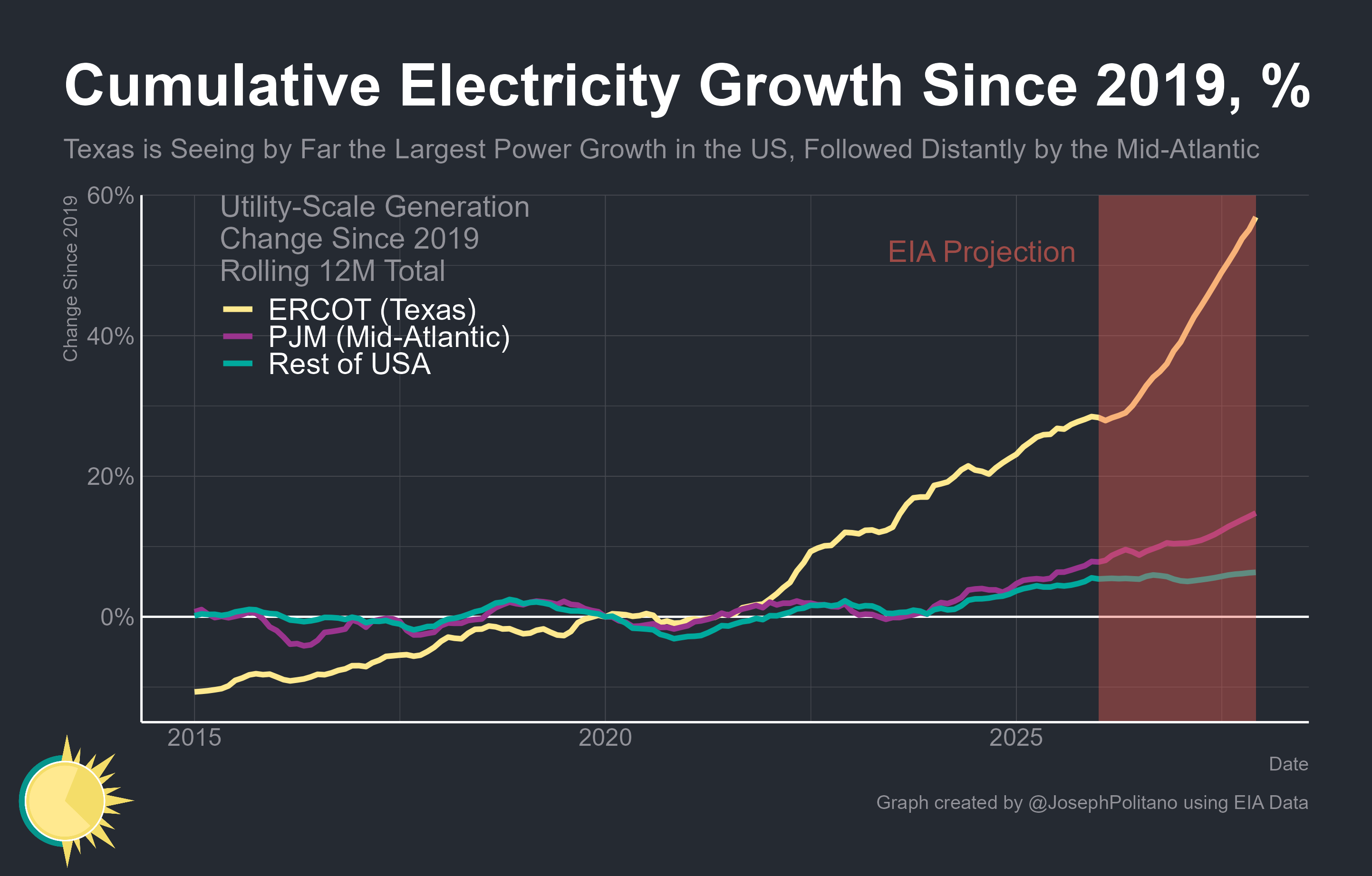

Indeed, Texas is seeing by far the fastest electricity growth of any region in the United States—total power generation in ERCOT, the state’s main utility interconnection, has already risen nearly 30% above pre-COVID levels and is projected to reach 57% above those levels by 2027. The PJM interconnection, which covers mid-Atlantic states from New Jersey to Virginia and is a major data center construction hub, is at a distant second place with less than 15% total growth from 2019 to 2027.

Natural gas will still meet the majority of Texas’ load growth over the next two years, but solar alone will cover 40% of new demand while wind will cover another 9%. That means solar will rise to 18% of the state's power by 2027, up from 12% last year and rapidly approaching wind’s 21%.

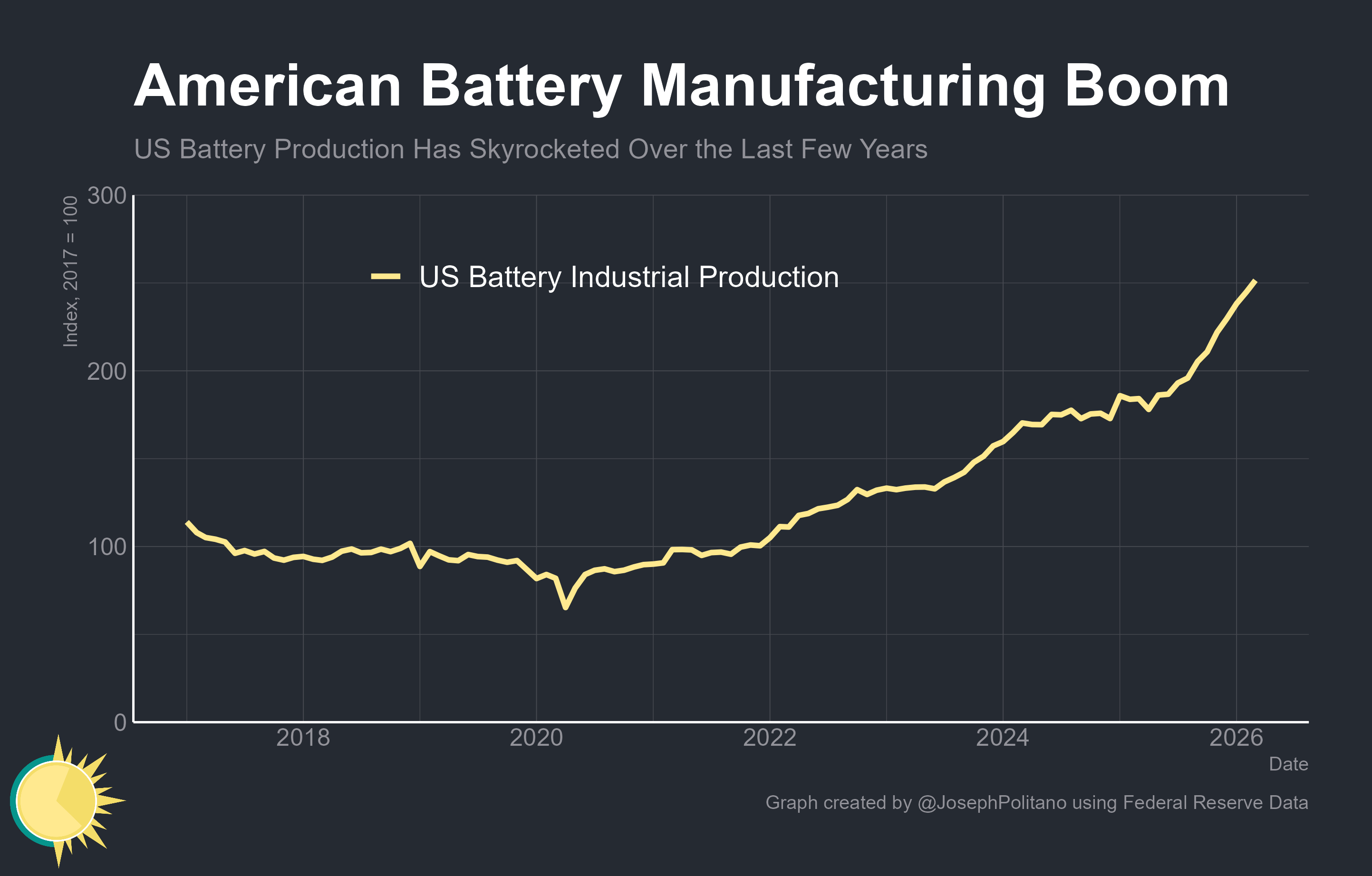

The rise in US solar and battery deployment has also had important effects beyond the direct investment in generation and transmission infrastructure—with major spillovers to the entire electrical supply chain and labor market. Most prominently, the US is in the midst of a massive increase in domestic battery production, with output rising 37% over the last year and tripling since late 2019. Many of those battery factories have been redirected from EV production, where adoption has slowed as federal incentives are cut, to utility-scale production. Overall, domestic output now meets the highest share of US demand in years, although the US is far from self-sufficient and net battery imports still totaled $19.6B in 2025.

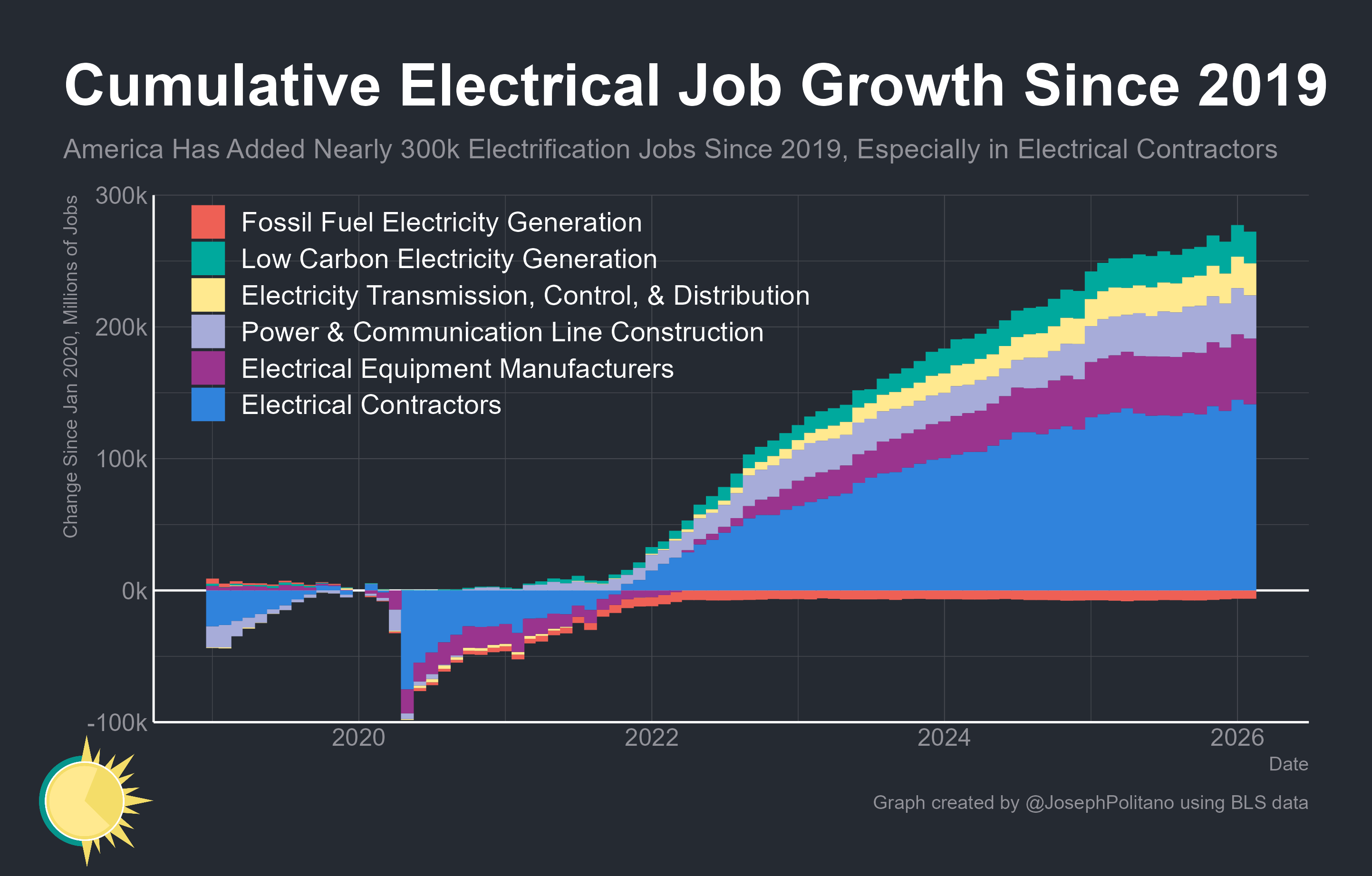

On the labor market front, while utilities have cut roughly 6k jobs at fossil-fuel generating plants since the end of 2019, they have added roughly 24k jobs at low-carbon non-fossil-fuel plants over the same time frame. Add in gains from the transmission, control, and distribution, and electric power utilities have added a total of 48k jobs. Power and communication line builders and electrical equipment manufacturers have also added 35k and 49k jobs, respectively, breaking out of an extended period of stagnation. Yet the largest growth has been among electricians and electrical contractors, where employment has risen nearly 150k to a new record high.

Conclusions

The rapid rise in AI-related data center power demand and its subsequent backlash have understandably dominated much of the recent public discourse around electricity investment. The fact that most major tech companies are now deciding to fund their own grid capacity proves just how important power access is to their gamble on AI development and how increasingly politicized energy consumption has become. Yet while AI development is a prime driver of current grid expansion, America was always going to need more power investment to meet this phase of economic growth and was already struggling to meet rising electricity demand well before the AI boom.

American manufacturing’s power consumption is poised to increase as factories built during the 2022-2023 construction surge come online. US EV adoption, while extremely slow compared to peer countries, has increased power demand and is still projected to rise significantly in the near future. Residential demand is gradually increasing as heating, cooking, and other appliances are slowly replaced with electric versions. Prices surged through 2021 and 2022 as those demand impulses hit a more supply-constrained environment. In other words, the costs of America’s electricity gap have only been mounting as power becomes more important to the national economy.

While the US still needs plenty of fossil fuels to keep the power grid running, the long-run growth trajectory increasingly lies in other power sources. Growth in domestic EV, battery, and solar production is high by historical standards, but it is still low compared to many of America’s peer countries, and the US is no longer a manufacturing leader in any of those industries. Having already fallen behind on production, the US risks multiplying the pain if it also falls seriously behind on deployment.

It is not a coincidence that some of America’s fastest-growing state economies, like Texas, are also among the fastest deployers of solar and batteries. They aren’t doing it primarily for climate or ideological reasons, but because it’s the easiest way to close their electricity gap and power economic growth. More of America will have to permit that kind of rapid energy buildout if they hope to meet their own increasing electricity needs.

Facing America’s rapidly growing AI-driven electricity demand, U.S. capacity expansion is still too slow.

In 2025, U.S. investment in clean energy, clean transportation, building electrification, and carbon management reached $278 billion, a record high. The problem is that, compared with China, this number still looks small. In the same year, China’s investment in clean-tech manufacturing and deployment reached $849 billion, about 3.1 times the U.S. level.

The structural difference is clear: the United States faces a demand curve growing faster than its institutional deployment capacity, while China faces an installation curve growing faster than its system absorption capacity.

The U.S. added 43.4 GW of solar, 24 GW of battery storage, and 11.8 GW of wind in 2025. But China is expanding at a completely different speed. In 2025, China added roughly 315 GW of solar, about 8 times the U.S. level, and around 119 GW of wind, about 10 times the U.S. level.

The United States is clearly seeing a boom in solar and storage construction, but it is still expanding within a relatively constrained institutional speed limit. China, by contrast, has entered an industrial-scale deployment phase in which several hundred gigawatts of new renewable capacity can be added in a single year.

This is the deeper difference. U.S. clean energy expansion is driven mainly by capital markets, state-level incentives, corporate PPAs, and private-sector demand. China’s expansion reflects a much more systemic mobilization: manufacturing capacity, grid investment, local governments, state-owned enterprises, private firms, supply-chain cost reduction, and national energy-security strategy all moving in the same direction.

America’s electricity gap is therefore not just a power-supply gap. It is also a national system-organization gap. The United States has technology, capital, corporate demand, and innovation capacity. But when it tries to convert these advantages into large-scale, low-cost, rapidly deployed infrastructure, it runs into permitting delays, interconnection bottlenecks, interstate coordination problems, transmission constraints, equipment supply-chain shortages, and political-cycle friction.

These are the problems the U.S. needs to solve quickly. Otherwise, if residential electricity prices rise sharply again, data centers and hyperscalers will almost certainly face large-scale political resistance from local communities. That is the biggest risk.

1.) Wjat is capacity? Real capacity should be thought of as the amount of power that can be generated over an extended period, a year, for example, with the plant running at the maximum rate consistent with long asset life.

Yes, many other things matter in generation, but, in discussion of supply meeting rapidly growing demand, what matters is the capacity discussed in the first paragraph.

2.) The chart in this piece shows the US adding no capacity, none, from coal or nuclear this year.

For context, the PRChina added >60% of total US coal capacity in just 14 months from Jan 2025 to Feb 2026. They added 1 Australia's coal generation capacity in just two months at the beginning of this year.

3.) Nameplate capacity, as is commonly used, is terribly misleading for energy sources with inherently low capacity factors. Solar in less favorable locations exemplifies this.

When one looks at real capacity, rather than illusory nameplate capacity, we see that coal was the number one source of new generation capacity in the PRChina in 2025. Yes. More real capacity was added than real capacity from solar.

The US hasn't built a new coal-fired power plant in ~15 years despite possessing enormous quantities of cheap coal.

4.) Batteries are not generation. They are fuel tanks. They add zero real capacity.

5.) When thinking about supply and demand over an extended period, it's useful to think about watt-hours, not watts.